Diversification of portfolio

What is a diversified portfolio?

The lower the correlation between the asset that I bring and the portfolio I already have, the more I stand to gain in terms of diversification. Let us suppose we form two portfolios. Portfolio number one. Here we are going to put the US, and Canada, and Germany, and the UK, and Japan, all very large stable developed countries and portfolio number two, we are going to put emerging markets. So we are going to put Mexico and Brazil, we are going to put Hungary and the Czech Republic, and we are going to put Indonesia and Malaysia. So we have a portfolio of developed markets and a portfolio of emerging markets.

Which portfolio is going to be more volatile?

Most people would guess that portfolio one will be, one of the developed markets would be far less volatile than portfolio two and that is the mistake of not thinking about correlations. Because the problem here is that each individual asset in the developing market portfolio has less volatility than each individual asset in the emerging market portfolio and these two things matter from the portfolios point of view.

The correlations across the developed market are far higher than the correlations across the emerging markets and that is a critical part of the risk of a portfolio. So, if you just think of the average volatility, then obviously the emerging market portfolio is going to be more volatile or far more volatile, than the developed market portfolio. If you take into account that these markets, the emerging markets are far less synchronized than developed markets are. That actually pulls the return of the portfolio quite a bit down. If you look at properly diversified developed markets’ equities portfolio, and a properly diversified emerging markets’ equity portfolio, yes you might find that this one is a little bit more volatile, but typically a lot less than most people would tend to think.

Let me illustrate this with the comparison between developed emerging and frontier markets. Emerging markets are not as large or not as liquid. As developed markets and frontier, markets are even one step below. For example, developed markets the US and Canada. Emerging markets Brazil, and Mexico, and Hungary, and the Czech Republic. Frontier markets, maybe Bulgaria, Romania or some other Latin American countries like, could be Bolivia relatively smaller markets in Asia and so.

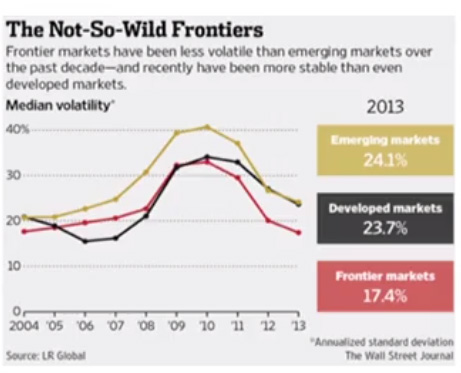

Most people would tend to think that developed markets are less volatile than emerging markets, and emerging markets are less volatile than frontier markets. That is typically the case, but here you have a recent article from the Wall Street Journal and it says “Investors Rewarded for Trek into Little Known Markets” and the little-known markets, this is basically an article about Frontier markets but here comes the interesting thing. Look at that picture that shows volatility over time of developed, emerging, and frontier markets and look at those numbers there. The volatility of a diversified portfolio of emerging markets in the year 2013, 24%. Developed market volatility in 2013, 23.7%. That is what the point that I was illustrating before is. Most people would tend to think that an emerging market portfolio would be far more volatile than a developed market portfolio. Well, look at what the data shows. In the year 2013, the emerging market’s portfolio was just a tiny bit more volatile than the developed market portfolio but look at the last number. Those frontier markets that are even more volatile than individual emerging markets. Well, they are more volatile than individual emerging markets, but they are also less correlated than developed markets and that the emerging markets. Therefore, look at that number 17.4. They are actually less volatile than a portfolio of emerging markets and less volatile than a portfolio of developed markets.

Look at that picture that shows volatility over time of developed, emerging, and frontier markets and look at those numbers there.

The volatility of a diversified portfolio of emerging markets in the year 2013, 24%. Developed market volatility in 2013, 23.7%. That is what the point that I was illustrating before is. Most people would tend to think that an emerging market portfolio would be far more volatile than a developed market portfolio. Well, look at what the data shows. In the year 2013, the emerging market’s portfolio was just a tiny bit more volatile than the developed market portfolio but look at the last number. Those frontier markets that are even more volatile than individual emerging markets. Well, they are more volatile than individual emerging markets, but they are also less correlated than developed markets and that the emerging markets. Therefore, look at that number 17.4. They are actually less volatile than a portfolio of emerging markets and less volatile than a portfolio of developed markets.

The volatility of a diversified portfolio of emerging markets in the year 2013, 24%. Developed market volatility in 2013, 23.7%. That is what the point that I was illustrating before is. Most people would tend to think that an emerging market portfolio would be far more volatile than a developed market portfolio. Well, look at what the data shows. In the year 2013, the emerging market’s portfolio was just a tiny bit more volatile than the developed market portfolio but look at the last number. Those frontier markets that are even more volatile than individual emerging markets. Well, they are more volatile than individual emerging markets, but they are also less correlated than developed markets and that the emerging markets. Therefore, look at that number 17.4. They are actually less volatile than a portfolio of emerging markets and less volatile than a portfolio of developed markets.

Now, of course, you would not expect that to be the case all the time. You would expect over a long period of time if frontier markets to be a bit more volatile than emerging markets, which in turn you would expect them to be a little bit more volatile than developed markets. But at the end of the day, because you need to think in terms of individual correlations and also, individual volatilities when you bring everything into a portfolio, sometimes the results may not be exactly what we expect. This is a quote from that article. It says individual frontier markets can be quite volatile, but as a group, there is a much lower correlation between them. So when you blend them together in a portfolio, you get much lower volatility and not so much about frontier markets, but about emerging markets, pulling in more or less in the same direction.

This article from the Financial Times “Fund Focus: Emerging Markets of the Future” says, if you look over the past ten years, taking this market individually, you will find that their volatility has been quite high. However, if you put them together into an index or a portfolio, then you find the standard deviation and the volatility tend to be very low because the correlation between the individual countries is also very low. So that is the key and a critical point to understand that when you are thinking about the risk of the portfolio, individual volatility is important, but correlations within the assets of the portfolio are just as important. That is the critical result in terms of diversification. So going back, keep in mind those three results that go to the heart of what diversification is all about. Result number one, that you have you know, minimizing risk sounds okay, maximizing returns sounds okay, but when you really think about it, you neither want to do one nor want to do the other. What you really want to do is to get the best possible combination of risk and return.

So result number one, diversification’s goal and the result is basically to get the possible, the maximum possible risk adjusted return. Result number two, that is what we get when we diversify. We will never get the highest possible risk-adjusted returns by putting all our money in one asset, or by putting all our money in the other asset. The maximum risk-adjusted return will always be somewhere in between when we are diversified and result number three is that the correlation. The lower the correlation, the better the risk of the portfolio, the lower the risk of the portfolio is going to be. So lower correlations help me diversify and lower the risk of the portfolio.

So remember two things:

- the critical concept of correlation that measures the sign and strength of two variables, which can be weak or strong, positive or negative. Remember this is not a statistical, boring mandate. It is absolutely essential from a practical point of view to understand and to build a proper portfolio.

- And diversification with the three points that we just highlighted, that it enables you to maximize risk adjust and return and whenever you’re thinking of bringing more assets into your portfolio from the point of view of reducing risk, the lower the correlation, the more you’ll be able to reduce that risk.

The CAPM, the model that we are going to use to calculate the cost of equity or the required return on equity is based on the beta. Beta is a measure of risk when you are properly diversified.