How do we calculate Beta (ß)?

What is Beta?

Beta is not only a widely used measure of risk but also, it is the central magnitude in what we call the capital asset pricing model. That capital asset pricing model that we also call the CAPM is one way of thinking about the expected or required return of an asset, given the risk of an asset and that risk of an asset is actually quantified by this beta.

Beta is a measure of relative risk but not a measure of relative risk in the way that we called the standard deviation before. The standard deviation, we say that we use it in relative terms. That is, we calculate a number that is for one specific asset and we use it to compare to the same number with other assets that as far as the relative comparison goes. However, basically, the number that we calculate is for one specific asset and for that asset only.

Why do we say that beta is a measure of relative risk?

Because the question that we are asking here is different. The question that we are asking here is how much an asset fluctuates relative to the market and so an asset can fluctuate more than the market or less than the market and that is why we call Beta primarily a measure of relative risk. Beta is a measure of relative risk from that perspective because we call it relative to the market.

Is this particular asset fluctuating more or fluctuating less than the market?

Now, those fluctuations have the reference value, which is equal to one and the reason the way we use the value of one is simply because if we have an asset that on average fluctuates just as much as the market, then we say that, that asset has a beta of one.

When the market goes up and down, why do we say that beta is a measure of relative risk?

Well, simply because the value of one tells me that the asset we are considering fluctuates just as much as the market. It does not fluctuate more, it does not fluctuate less, on average over the relatively long period of time. Therefore, an asset with a beta of one may actually go down when the market goes up and that does not seem to respond to the measure or to the idea of a beta equal to one. But again, what we are seeing is that what is the average fluctuation of an asset over the long period of time relative to the market. Therefore, on any given day, week, or month, anything can happen. But if you look at this over a sustained period of time, then an asset with a beta equal to one will fluctuate more or less, that, just like the market. That means that, on average, when the market goes up and down 1%, then you would expect these assets to go up and down 1% just like the market does. Now of course, that gives you an idea of what are the complements, that is, what is a beta higher than one and what is a beta lower than one.

Beta a symmetric measure of risk

A Beta higher than one is an asset that actually magnifies the fluctuations of the market and that basically means that as the market goes up and down 1% this particular asset will go up and down more than 1%. Now it is important to understand that we call sometimes Beta a symmetric measure of risk and what we mean by symmetric is basically the following. Let’s suppose, let’s take an, a Beta, an asset with a Beta of two. An asset with a Beta of two means that on average when the market goes up 1%, this asset will go up more than the market that is 2%. But when the market goes down 1%, this asset will also amplify the downfall, and it will go down by 2%. So a beta larger than one magnifies the risks but also magnifies defaults. And so the higher the beta, and particularly the higher the beta relative to one, then the more that this particular asset is going to magnify the fluctuations of the market. Now you can guess what a beta less than one actually indicates. It is an asset that mitigates the volatility of the market. And that basically means, let’s suppose that the market goes up and down 1% over a given period of time, well an asset with a beta of 0.5 would basically go up in half and down in half relative to the market. So when the market goes up and down 1%, this asset will go up half a percentage point. When the market goes down 1% this asset will go down 0.5%. That means that this market will tend to mitigate the volatility of the market.

And now, we are going to go back one more time to our data, and we are going to look at those Betas.

| Year | USA | Spain | Egypt | World |

| 2004 | 10.7% | 29.6% | 126.2% | 15.8% |

| 2005 | 5.7% | 4.9% | 161.6% | 11.4% |

| 2006 | 15.3% | 50.2% | 17.1% | 21.5% |

| 2007 | 6.0% | 24.7% | 58.4% | 12.2% |

| 2008 | -37.1% | -40.1% | -52.4% | -41.8% |

| 2009 | 27.1% | 45.1% | 39.7% | 35.4% |

| 2010 | 15.4% | -21.1% | 12.4% | 13.2% |

| 2011 | 2.0% | -11.2% | -46.9% | -6.9% |

| 2012 | 16.1% | 4.7% | 47.1% | 16.8% |

| 2013 | 32.6% | 32.3% | 8.2% | 23.4% |

| AM | 9.4% | 11.9% | 37.2% | 10.1% |

| GM | 7.6% | 7.9% | 21.4% | 7.7% |

| SD | 17.9% | 28.1% | 64.0% | 20.1% |

| Beta W | 0.9 | 1.1 | 1.5 | 1.0 |

And If you actually look at those Betas, there is something there that shouldn’t be too surprising. And that is, the U.S. is a very large market. In fact, the U.S. is about 45% of the world market that you have at the very end, and therefore, of course, you would expect that the U.S. is going to actually react and sort of determining the fluctuations of the world market. So, you would expect for such a large asset relative to the world market that the beta should not be too different from one and as you can see there, the beta of the U.S. market is 0.9. That means that the U.S. market tends to mitigate a little bit the annual fluctuations of the world market.

The opposite is the case of Spain, but again, not by a very large magnitude. The beta of Spain relative to the world market is 1.1, and that basically means that when the world market goes up and down, 1%, while the Spanish market tends to amplify a little bit the rises and tends to amplify a little bit the decreases of, of the market. But look at the 1.5 Beta of Egypt. That is very typical of an emerging market. It actually amplifies quite a bit the rises of the world market, when the world market goes up, the Egyptian market goes up 50% more, but it also amplifies the falls of the world market. When the market, when the world market goes down by 1% on average over the long term, then the Egyptian market tends to go down by 1.5%. So, that is not surprising, and it’s actually sort of the typical behavior of emerging markets. They tend to go up by more than the world market when the world market is rising and they tend to fall more than the world market when the world market is actually falling, and that is precisely what beta is designed to capture. Now, we are, we are going to discuss the calculation of these betas, again, in the technical note. But as a matter of fact, there’s an even better shortcut that we can get. And the better shortcut that we can get is that you can find betas everywhere. You can go to Yahoo Finance, you can go to Google Finance, you can go to Bloomberg and any of these would actually give you the beta of any company over the next three to, excuse me, over the last three to five years. And the fact that these betas are actually publicly available helps you a lot. Because you do not have to bother with calculating this.

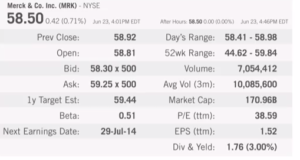

So let us take a look, for example, at this and I want to highlight two things with this one, this is just a little screen shot from Yahoo Finance. And what I want to show you there. This is actually from late June. And this screenshot actually shows you quite a bit of information about a company called Merck, a pharmaceutical, large diversified company.

A pharmaceutical company is a type of company that sometimes we call defensive. Defensive basically means that when the economy is actually growing a lot or contracting a lot, well, this company is still doing more or less well, because we don’t choose to buy medicine, we don’t choose to buy many of the things that this company produces. Sometimes we have to. Whether the economy is doing well or the economy is doing poorly and so, companies like Merck, large, diversified, pharmaceutical companies. They tend to be defensive and in terms of beta, that basically means that their betas tend to be lower than one. And if you actually look at the beta of Merck at this particular point in time, measured over the last few years is actually 0.5. That is very consistent with a pharmaceutical company. When the market goes up and down 1%, this particular company goes up and down half as much as the market does. So it doesn’t go as fast and as high as the market, but it doesn’t fall as fast and as high than the market. Now compare that with Google. And Google, this is again, this screen shot is taken from Yahoo Finance. It is on exactly the same date, just a few minutes later. And again, you have some information about Google which you might find more or less interesting, but the number I want to highlight is that beta. And that beta is 1.14, let’s round it up to 1.15. That basically says as you would expect from a technology company that is going to actually magnify the market fluctuations. Technology companies typically, yeah, more often than not, tends to be the case of when the market goes up, these companies tend to go up by more. But when the market goes down, these companies also tend to go down by more. So basically we have two companies, two betas. And what I wanted to highlight was two things.

A pharmaceutical company is a type of company that sometimes we call defensive. Defensive basically means that when the economy is actually growing a lot or contracting a lot, well, this company is still doing more or less well, because we don’t choose to buy medicine, we don’t choose to buy many of the things that this company produces. Sometimes we have to. Whether the economy is doing well or the economy is doing poorly and so, companies like Merck, large, diversified, pharmaceutical companies. They tend to be defensive and in terms of beta, that basically means that their betas tend to be lower than one. And if you actually look at the beta of Merck at this particular point in time, measured over the last few years is actually 0.5. That is very consistent with a pharmaceutical company. When the market goes up and down 1%, this particular company goes up and down half as much as the market does. So it doesn’t go as fast and as high as the market, but it doesn’t fall as fast and as high than the market. Now compare that with Google. And Google, this is again, this screen shot is taken from Yahoo Finance. It is on exactly the same date, just a few minutes later. And again, you have some information about Google which you might find more or less interesting, but the number I want to highlight is that beta. And that beta is 1.14, let’s round it up to 1.15. That basically says as you would expect from a technology company that is going to actually magnify the market fluctuations. Technology companies typically, yeah, more often than not, tends to be the case of when the market goes up, these companies tend to go up by more. But when the market goes down, these companies also tend to go down by more. So basically we have two companies, two betas. And what I wanted to highlight was two things.

- Betas, you do not really have to bother calculating them most of the time. You can actually find them in, again, Yahoo Finance, Google Finance, many publicly available sites.

- They will depend on the nature of the business, on the nature of company we’re dealing with.

Pharmaceutical companies, they tend to be large, they tend to be stable, they tend to mitigate market fluctuations. Technology companies, they tend to be more volatile than the market, and that is reflected in their betas.