What is Diversification?

Diversification

The goal of diversification

The ultimate goal of diversification is to maximize, to get the highest possible risk-adjusted returns.

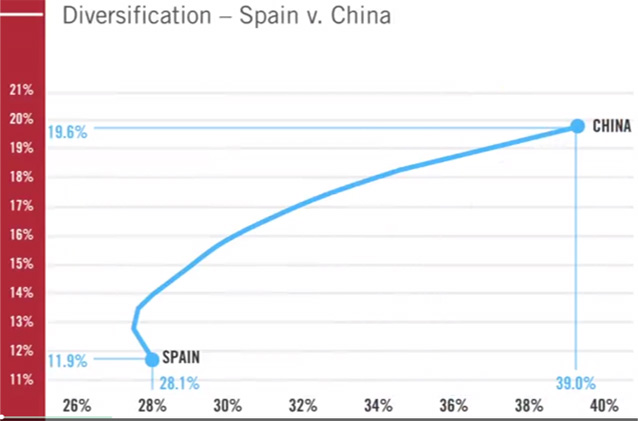

When I do diversify a portfolio, would I obtain as a result is a possibility of choosing the combination that gives me the highest, Risk-adjusted return? So, not only the goal of diversification is obtaining the highest possible risk-adjusted return. The result of diversification is obtaining that highest possible risk-adjusted return and I want to illustrate this by putting together an emerging market and a developed market. We have taken Spain as an example of a developed market and China as an example of emerging market.

This picture actually is built on the behavior of the Spanish market and the Chinese market over the last ten years, between 2004 and 2013. The Spanish market generated a mean annual return of 11.9%. The Spanish market also generated a volatility of 28.1%. The Chinese market generated a mean annual return of 19.6% and the volatility of the market, over there, the Chinese market over that period was about 39%. So, look at the point that is actually labeled Spain. If I had put all my money in Spain, over the last ten years, then my mean annual return would have been 11.9% and my volatility would have been 28%. If I had put all my money in the dot in the point labeled CHN China then my mean annual return would have been 19.6%, and my volatility would have been 39 percent.

As we are talking about diversification; therefore, what really matters is combining the Spanish market and the Chinese market and for that, we need to keep one thing in mind that is the correlation, which is 0.6. That is actually not an extremely high correlation but it is positive which means that in the long term Spanish market and the Chinese market tend to move more or less together. Not very closely related but more or less in the positive direction and that means that both of them in the long term they tend to go up. The blue line is basically different combinations of the Spanish market and the Chinese market. So the first point to the left and above Spain is a combination in which you invest 90% of your money in Spain and 10% of your money in China. That 90%, that 90 10% combination between Spain and China actually gives you a return and a risk of that portfolio, and that is identified by that dot. As we move, actually to the right and above, then we are basically decreasing the proportion of Spain in the portfolio and increasing the portfolio of China. So let’s look now at the first point to the left and below the CHN point. That is a portfolio that is invested 90% in the Chinese market and 10% in the Spanish market. So all those infinite points in fact along the blue line are what we call feasible portfolios are portfolios that I could have built, that I could have had by combining the Spanish market and the Chinese market. All right. Now let’s look at a couple of important points along that blue line. Point number one, that I want to highlight is that one. The point that goes furthest to the left and if you look actually at the bottom line, what we are measuring on the horizontal axis is a risk and that means that the point that goes furthest to the left is of all the possible combinations between Spanish market and the Chinese market. We get the combination that gives the lowest possible risk and in our case, that is the lowest possible volatility.

For example, in that particular case, that is 87% in Spain and 13% in China. If I had invested over the previous ten years 87% of my money in Spain, and 13% of my money in China that would have given me the combination between these two markets that would have led to the lowest possible risk measured in terms of volatility. That actually would have enabled me to let’s say, the Spanish investor, to reduce risk from 28.1% to 27.8%. A little bit not much, but it is a reduction in risk and that reduction in risk came at the same time with an increasing return. If I had been solely invested in Spain, my mean annual return would have been 11.9%, but because I put 13% of my money in China, my mean annual return was actually higher 12.9%. So, if I am a Spanish investor that diversified into the Chinese market, and decided to put 87% of my money in Spain, and 13% of my money in China. I won two ways. I won because my risk is a little bit lower, and I won because my return has actually been higher. So I win in, in two different dimensions, I have lower risk, but I also have a higher level of return.

You can always find people that say look, I have been investing in my own market forever, and I can take the volatility of that market. I am kind of used to the volatility of that market. Well, that is not a reason for not diversifying and the reason for that is, let’s look at this other green point. That other green point is actually roughly 74% invested in Spain, and 26% invested in China and by construction, that particular portfolio has the same volatility as the Spanish market. So that, what that means is that if I had had over the last ten years, 74% of my money invested in Spain, and 26% of my money invested in China, the volatility of that portfolio would have been 28.1%, which is exactly the same volatility that it would have had if I had been fully invested in Spain. However, you can see what the difference is. The difference is that my mean annual return would have been 2% points higher, 200 basis points higher by being properly diversified. So this is like a free lunch. In fact, diversification is what sometimes we call in finance the last free lunch that you can find in markets. Because in this case by going out of Spain and investing part of my money in China about a quarter of my money in China, and three-quarters of my money in Spain. I ended up with a portfolio that has the same level of risk, but a higher level of return than putting all my money in, in Spain. So this is a reason for diversifying. We can get a little bit of a free lunch, and it is easy to explain why the Spanish investor is always better off. Because in the first point, he reduces risk and increases return and, in the second point, he gets the same level of risk, and gets a, a higher, an even higher return. Now, it is a little bit more difficult if you look at that picture to sell diversification to the Chinese investor and, the reason it is a little bit more difficult, it is because you cannot offer.

Notice that if we move from the point labeled CHN to the first point to the left and below, at that point, we are reducing the risk of the portfolio, but we are also reducing the returns. So, now we face a trade-off. The Chinese investor can get actually a lower level of risk by diversifying into Spain, but it is the sacrifice of that the cost of that is expecting lower returns. That did not happen to the two points that we had seen before in Spain, you know in, in the two points, in the two diversification strategies that we have seen before this Spanish investor in one. He won two ways, by reducing risk and increase in returns and in the other, he was not wearing soft in one way, in terms of risk, but was much better off in terms of return.

Well, unfortunately we cannot offer that for the Chinese investor. Does that mean that there is no way to convince the Chinese investor that he should diversify in Spain? No, it does not mean that and the reason is, let’s look at these numbers here.

The first two columns are proportions of our money invested in the Spanish market and in the Chinese market and notice that if you go line-by-line, all those first two weights always add up to one. So in the first case, I have all my money invested in Spain and nothing in China. In the last case, I have all my money invested in China, and nothing in Spain. And then in the second case, if I have 90% of my money invested in Spain then I have 10% of my money in China. Whatever I do not invest in one market, I invest in the other. So the sum of those two weights is always going to be equal 1. Which means my portfolio is always fully invested.

The next two columns return and risk are the numbers that generated the blue line in the picture that we have seen before. So, that blue line that you are seeing now again has been generated from the two numbers, that we labeled return and risk in this particular picture. So that is another way of saying that is that, each portfolio each combination of the Spanish market, in the Chinese markets gives me a return and a risk that is consistent with that particular portfolio.

Now, we were thinking about ways of convincing the Chinese investor that he needs to diversify, too. Now, the last column is basically the third column divided by the fourth. So for example, if I divide 11.9 by 28.1 then I get 0.424. If I divide, I am going to the very end now, 19.6% by 39%. I get 0.503. So, if I divide the return column by the risk column, I get the last column which RAR and that RAR is basically risk-adjusted return. There are much more technical and better ways of looking at risk-adjusted return but by putting one divided by the other. What investors want at the end of the day is to get the highest possible risk-adjusted return.

In this particular case, if you put 40% of your money in the Spanish market, and 60% of your money in the Chinese market, then you actually will maximize. The combination of risk and return of the Spanish market and the Chinese market. I could show you mathematically that you will never find that maximum risk-adjusted return, by putting all your money in Spain, or by putting all your money in China. In other words, if you try to find the highest possible risk-adjusted return it is always going to be somewhere in between and being somewhere in between means that you are splitting your money between the two markets. It means that you are diversifying. It is a very important result. If I am combining two assets, and the correlation of those two assets is any number lower than one, and remember that in this case is .6, I will never get. The highest risk-adjusted return by putting all my money in one market or by putting all my money in the other market. I will always find the highest risk-adjusted return by putting my money somewhere in between and in this particular case, it happens to be, 40 60 in some other cases maybe 90, 10 or 25, 75. It does not really matter but it is never going to be all my money one market and no money in the in the other market.