Project Evaluation

As you will remember that cost of capital is the minimum required return on the company’s investments and now we will discuss a little bit about how to build that cost of capital into a rule to decide whether you should go ahead with the project or not. Also, we will discuss the two most widely used tools, for evaluating projects which are NPV (Net present value) and IRR (Internal rate of return).

Here are few questions that we will answer in this session:

Having estimated a company’s cost of capital, do we need to do anything else as, as a discount rate or, or we’re done with that?

Are we done, has estimated the cost of capital of Starbucks at 7.2%, or do we need to think about, maybe, having different discount rates for different divisions or different countries or different discount rates over time?

Why do we need to evaluate projects?

It is important that you keep in mind that in order to make investments, companies need capital and that capital needs to be provided by someone and that someone requires a return. And that return will be tied, will be linked to the risk that this capital provider perceives on the company to which he is lending that capital. So on the one hand, someone has to provide that capital that capital has a required return, and that required return is associated with risk, which means that the company already has a restriction. The restriction is that they need to deliver the type of return that the investors are expecting. Of course, they do not need to do this every day, every week, or every month, but eventually, they need to deliver the return that is provided by the or the return that actually comes with the risk that, investors are bearing for providing capital to the company.

The second important thing about this, remember, the capital is scarce and as any scarce resource, we have to invest it wisely and invest it wisely means that we need to get a return out of that capital which is higher than the cost of providing that capital. And at the end of the day, that is what project evaluation is all about, is comparing the return from our investments, from our capital investments, the return that we expect because returns are always in expectations. Anything that comes in the future is something that we expect. We will never know and we will talk a little bit more about that but we need to compare the return that we expect from the capital invested with the cost of that capital.

Again, someone is providing that capital, the capital provided expects a rate of return, and that rate of return actually has to be delivered by the projects and by the company investing in those projects. So, from the point of view of the capital itself, what is important is to keep in mind that capital is scarce, that it needs to be, allocated in an appropriate way, and at the end of the day, when we do that, we’re creating not only private value, but also social value.

Now, if you flip the coin, then we can say actually that in the other way around. Which is if you do not invest your capital wisely, then you will be destroying private value, but you will be also destroying social value because you are misusing capital, you are using capital, getting a return out of it, which is lower than the cost of providing that capital.

So point number one, we need to evaluate projects to make sure that we use the capital wisely. The general idea is that we don’t want to misuse the capital, we don’t want to do that from a private, corporate point of view, we don’t want to do that from a social, point of view either.

In order to, to evaluate the projects, we need to determine two things:

- We need to determine for any given project whether we should go ahead or not with it. And in order to do that, basically we’re going to be comparing what we expect from the project and, we’re going to be discounting that at a rate. Or we can actually look at the return of the actual project and compare that to a discount rate.

- Which one we should go ahead with if there is more than one project.

Either one way or the other, if we focus on one individual project, the question will be should we go ahead with this project or not? Now, of course, there may be more than one projects and, as a matter of fact, companies always are thinking of new things in which to invest their capital and sometimes because, again, capital is scarce, we need to decide which project we’re going to invest in and which projects we’re not going to invest in. Sometimes people call these competitive projects.

What do you do when you have more than one project, but, you know, you have a capital restriction?

How do you decide whether you go for this one or for that one?

How do we evaluate projects?

The two main tools to evaluate projects are NPV and IRR. NPV stands for Net Present Value and IRR stands for Internal Rate of Return. And, of course, you know, pretty much like the CAPM for the cost of equity, it is not the only model, but it’s the most widely used.

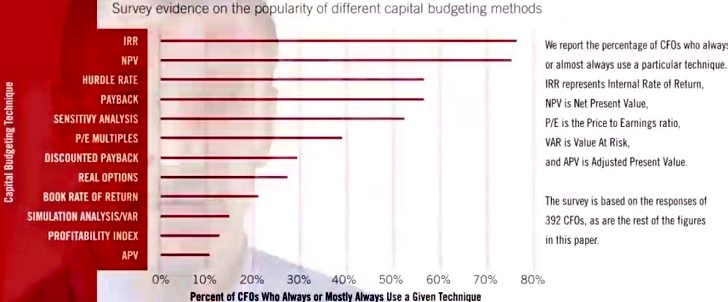

Well, if you take a look at this picture, then you’ll see that IRR and NPV are not the only two tools that we can use to evaluate projects, but they are by far the most widely used of all the tools that we actually know. It is important that you keep in mind, again, in finance, we always have a choice of tools and, and some tools are more widely used than others are. But at the end of the day, what is important is first, how plausible is the tool that we’re using, to understand how we use it, and then to be able to implement it properly. And that’s basically what we’re going to do in this session with these two widely used tools, NPV and IRR. So keep in mind again, the same thing that we highlighted with the CAPM, that is, these are not the only two tools to evaluate projects. They have pros and cons as any other tools. And, but we’re going to focus on these two because they are easy to understand, they have a very clear intuition underneath and, more important than anything else is that they’re both very widely used. And there’s a good reason why they’re widely used. They’re internally consistent, they are methodologically correct, particularly the net present value, then we’re going to see that there are a few problems that we need to, actually discuss related to the IRR.